Albania and the Geopolitics of the Trans-Adriatic Pipeline: Regional and Domestic Dimensions

[author title=”Patrick McGrath” image=”/wp-content/uploads/2021/11/patrik.jpeg”]Tufts University Graduate Student | IDM’s summer intern 2018 [/author]September 2018 – The Southern Gas Corridor (SGC) initiative was launched by the European Union (EU) in 2008 with the aim of developing a new supply route for Caspian and Middle Eastern gas to European markets and reducing the EU’s dependence on Russia as its primary supplier. The 3,500 km corridor will deliver 10 billion cubic meters (bcm) of gas per year from Azerbaijan’s Shah Deniz II field upon completion in 2019-2020 but expand in subsequent years with infrastructure extensions and connections to Central Asia.[1]

The SGC is composed of three primary segments: the South Caucasus Pipeline (SCP) from Azerbaijan to Georgia, the Trans-Anatolian Pipeline (TANAP) from Georgia to Turkey, and the Trans-Adriatic Pipeline (TAP) from Turkey through Greece, Albania, and Italy. As the final link between the EU and the Middle East, TAP has highlighted the complex geopolitics behind energy security in Europe today and has far-reaching implications for Southeastern Europe (SEE) and Albania in particular, which faces a future as a regional energy hub.

This article will explore the key issues at stake to understand the primary interests and challenges embedded in TAP across SEE and Albania specifically. It will first discuss the regional impact of TAP in the areas of integration, diversification, conflict, and competition and then assess the security, economic, and political effects of TAP within Albania. While the approaching completion of TAP promises substantial benefits and opportunities for the region, it is likely to also spur novel challenges and far-reaching conflicts.

Regional Pipeline Politics: Partnerships and Rivalries

Internal and external integration: As part of the SGC, TAP’s initial conception was based on the need to integrate regional energy markets and infrastructure within the SEE region and link pan-European gas networks. The EU lists the SGC with its three component parts among its list of Projects of Common Interest, highlighting the potential to deliver new sources of gas to EU member states.[2] TAP will provide multiple linkages between SEE states with the EU and thereby diversify supply routes across Europe.

Within SEE, TAP has offered a number of opportunities to connect neighboring states through a unified energy network, and two major projects are currently underway that aim to take advantage of future transmission lines from TAP to Albanian networks. The most significant initiative is the Ionian Adriatic Pipeline (IAP), a 511 km pipeline with a capacity of 5 bcm/year that would connect Albania with Montenegro, Bosnia and Herzegovina, and Croatia.[3] The four countries signed an agreement on the development of the pipeline in 2016 and agreed in 2018 to form a separate company to implement the project.

The second regional project under development is the Albanian-Kosovo Gas Pipeline (ALKOGAP), a 255 km pipeline with a capacity of 1.12 bcm/year between Albania and Kosovo.[4] Both projects would present major advancements in energy security and regional connectivity, promoting the concept of the cross-regional Gas Ring backed by the Energy Community.

TAP’s most direct impact on the region will thus be as a means to enhance regional integration and likely stimulate further cooperation in infrastructure, security, and legal harmonization.

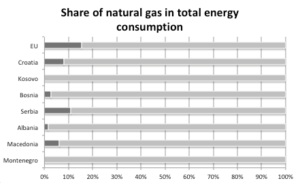

Diversification through new supplies and suppliers: TAP has been championed by the EU as a means to promote diversification by seeking both new energy sources in SEE and new energy providers. In the area of supplies, SEE states consume far less natural gas compared to the EU average around 20%.[5] Albania, Kosovo, and Montenegro are effectively non-gasified, while natural gas makes up less than 10% of consumption in Bosnia, Croatia, and Macedonia.[6] TAP will provide the opportunity to gasify the region through spur lines and increase flows to countries with limited access.

To this end, Albgaz – Albania’s public company established to manage domestic gas distribution and transmission – signed an agreement with the local subsidiary of Azerbaijan’s state-owned oil company in February 2018 to design a pipeline with the capacity of 1 bcm/year from Fier to Vlorë, allowing for the transmission of gas from TAP.[7] TAP will thus have a positive impact on boosting the region’s energy security and provide a much-needed opportunity for infrastructure upgrades and extensions. However, this will increase the region’s dependence on hydrocarbons at the expense of more sustainable sources, particularly in Albania.

More significant for the EU is the diversification of suppliers and supply routes, and TAP and the SGC present a shift both away from Russia and toward the Caspian region. The EU has made reducing its dependency on Russia a perennial priority, particularly since the 2009 halt in Russian gas flows through Ukraine. Despite the controversial construction of Nord Stream 2, TAP will challenge the dominance of Russia’s state-owned gas company Gazprom in European markets.

To pivot suppliers, the EU has turned toward the Caspian region, with agreements to develop energy infrastructure in Azerbaijan, Turkmenistan, Uzbekistan, and Kazakhstan. To secure the region’s involvement, the EU granted the Shah Deniz II consortium exclusive 25-year access to the SGC’s initial capacity of 10 bcm/year.[8] However, this pivot has not gone unnoticed by Moscow, and Gazprom has stated an interest in bidding for a share of the SGC’s future capacity in open auction, thereby potentially regaining Russian energy dominance. The EU’s turn toward Central Asia also risks challenging the increasing clout wielded by China, which has sought to capitalize on the region’s energy supplies through its Belt and Road Initiative.

Despite promising developments, such as a possible pipeline from Turkmenistan to Azerbaijan following the signing of the Caspian Sea Convention this summer, the EU risks stoking tensions among new suppliers. Critics have also raised doubts about the viability of the project, with low gas prices threatening the SGC’s profitability, concerns about the size of Azerbaijan’s hydrocarbon reserves and its appeal as a partner, and the prioritization of political over economic considerations. TAP will thus pull SEE further into geopolitical conflicts and expose the region to the volatility of disputes between the EU, Russia, and China.

Managing regional conflicts: TAP has revealed both the potential for opportunities to enhance regional cooperation and the risks for local rivalries to derail the project. A number of proposed pipeline projects in SEE over the years, including Nabucco and South Stream, have left SEE states such as Greece, Romania, Bulgaria, Croatia, and Serbia vying for the political and economic dividends of a pipeline through their territories.

TAP’s final route has proved a boon to countries that have taken advantage of the opportunity for secondary projects, such as the Interconnector Greece-Bulgaria, which will transport gas from TAP into Bulgaria. Conversely, Serbia has confirmed the construction of an alternative Serbian Stream pipeline that will deliver gas from Russia and thereby increase the region’s dependence on a single supplier. Rather than viewing TAP as a mutually beneficial asset, SEE states have largely approached energy security as a zero-sum game.

Additionally, TAP will likely see competition from the introduction of liquefied natural gas (LNG) in the region. The most significant leader in this area is Croatia, with its plans for the Adria LNG regasification terminal in Krk, while discussions have taken place for a terminal in Albania. A shift toward LNG sources, particularly with the backing of new suppliers such as the US and Qatar, would challenge the strategic relevance of TAP and Albania as the entry point for regional gas flows.

The region has also witnessed two new challenges to cooperation from states along the pipeline’s route: the slide toward authoritarianism in Turkey and the formation of a populist government in Italy. Turkey had previously been viewed as a key ally in the SGC, providing a vital route for non-Russian gas to the EU. However, the country’s democratic backsliding and increasing hostility toward the West have pushed it further toward an alliance with Russia and raised concerns about its reliability. The most significant evidence for this change is TurkStream, a new pipeline that will transport gas directly from Russia to the EU through Turkey, thereby undermining the utility of the SGC.

In Italy, the populist coalition that entered into power in 2018 – and particularly the Five Star Movement (M5S) – campaigned on a platform opposing TAP and advocating for closer ties with Russia. In June 2018, Italy’s Minister of the Environment called TAP “pointless,” and a strong No TAP activist network has formed in opposition to the pipeline.[9] The US and the EU have pressured the M5S to relax its criticism of the project, but TAP remains a contentious issue in Italy, despite recent assurances from President Sergio Mattarella.

It seems likely that the EU and its partners will be able to exert sufficient pressure to ensure the Italian government backs TAP, although this is likely to cost M5S domestic support in favor of its coalition partner, the League. The downward-spiraling relationship with Turkey, however, appears far harder to resolve – especially with the country’s standoff with the US this summer – and the EU may soon perceive Turkish routes as equally risky to those from Russia.

The rise of EastMed: The 2009 discovery of the Tamar gas field in Israeli territorial waters ushered in the beginning of a new theater for global energy politics: the Eastern Mediterranean. This discovery set off a series of findings across the area, including the Leviathan field in Israel, the Aphrodite field in Cyprus, and the colossal Zohr and Noor fields in Egypt. Israel, Cyprus, Lebanon, and Egypt now appear poised to take on a major role in global energy markets as they begin to tap the new fields, build up infrastructure, and seek markets for export.

The most significant challenge for the region is how to deliver its gas to European markets. One option is conversion to LNG and export by ship, and Israel has led the way by signing an agreement to use Egypt’s two previously dormant LNG liquefaction plants, although Egypt’s own discoveries will require additional capacity. A second option is the construction of a new pipeline. The less expensive version would go by land, traveling through Syria and Turkey into the EU, but this option has proved unlikely given the war in Syria and worsening relations with Turkey. Consequently, Italy, Greece, Cyprus, and Israel signed an agreement in December 2017 to back EastMed, a 1,300 km underwater pipeline transporting gas from Cyprus to Greece with a capacity of 12-16 bcm/year.[10]

The emergence of this group of energy producers and the probability of bypassing Turkey has given rise to a new regional bloc, with Israel, Egypt, Cyprus, and Greece confronting Turkey’s regional energy hegemony. The tension has worsened regional relations, with Turkey and Greece recently clashing over a series of disputed Aegean islands and Turkey seeking to block the exploration of Cypriot territorial waters that it claims belongs to the breakaway Turkish Republic of Northern Cyprus.

The impact of EastMed on TAP is still unclear since it remains largely in planning stages, but the most probable impacts are a reduction in the relevancy of the SGC as an alternative to Russian gas as well as a worsening of EU relations with Turkey as tensions escalate with EastMed suppliers.

TAP in Albania: Profits and Pitfalls

TAP is certain to impact Albania in a number of different areas, providing lucrative opportunities and new challenges for politicians. Although Albania’s inclusion in the project has been largely a consequence of its fortunate geographic location, the country has sought to capitalize on possible spillover benefits but has paid less attention to potential costs.

The single greatest impact of TAP on Albania will be as a means to enhance its energy security and diversify energy sources. Albania consumes effectively no natural gas, and thus the plan to connect TAP to a national gas network will provide the opportunity to adopt gas as a source of domestic consumption. Albania has historically struggled with an inefficient overreliance on hydropower that, while environmentally sustainable, has proved to be insecure and subject to changes in weather. Additionally, natural gas is expected to be cheaper than hydroelectric power, thereby reducing household costs and helping prevent blackouts. Finally, the investment in infrastructure and an improved business climate may stimulate further developments in Albania’s own onshore and offshore hydrocarbon reserves, which are substantial and largely unexploited.[11]

Albania’s government has emphasized both the direct and spillover economic benefits of TAP in areas such as construction, communications, manufacturing, utilities, trade, and business services. TAP will have both quantifiable impacts, including in employment, procurement, investment, and tax revenues, as well as more intangible effects, including in improved integration, greater foreign investor confidence, knowledge transfer, and more reliable energy supplies.

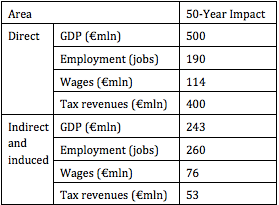

A report by Oxford Economics predicts a contribution of €500 million to GDP over TAP’s 50 year lifecycle (€157 million during construction, €8 million for each year of operation) and €400 million in total tax revenues.[12] It also forecasted an average of 2,900 annual jobs during construction and 190 jobs for each year after, along with the provision of €114 million in incomes over 50 years.[13] Last, it predicted €175 million in indirect contributions and €68 million in induced contributions over 50 years through stimulation of the local economy and procurement.[14] TAP’s investment of €60 million in Albania’s road infrastructure will provide an additional contribution.[15]

The greatest intangible benefit for Albania will likely be the perception of an improved investment climate, potentially paving the way for increased foreign investment. The greatest economic costs of TAP for Albania will be in the area of the environment, due both to potential damage to agricultural land as well as increased carbon emissions.

TAP has also had a number of political ramifications for Albania both domestically and in its foreign relations. TAP’s construction has boosted Albania’s power as a regional hub for energy and has ensured its status as an indispensable partner for future projects, including ALKOGAP and the IAP. It has especially served to enhance Albanian-Croatian relations, as the two countries seek to cooperate in dominating the region’s energy supply routes. TAP has also boosted Albania’s importance and reliability for the EU, as it will now provide a crucial link in the SGC. Conversely, this increased importance for the EU may limit Albania’s foreign policy options and draw it into distant geopolitical conflicts.

Domestically, TAP has seen steady non-partisan support from the Albanian government. However, the construction of TAP has generated political pushback from farmers along TAP’s route in Albania whose land was expropriated. Reports have documented complaints about inadequate compensation, administrative irregularities, and a lack of transparency in payments.[16] Critics have also pointed to potential environmental risks as well as harm to biodiversity and cultural heritage.

Nevertheless, TAP has been first and foremost a win for domestic politicians who have taken credit for associated economic and political gains.

Looking Ahead

From its very inception as a tool to combat the weaponization of energy by Russia, TAP has cast a spotlight on the dynamic geopolitics of energy security in Europe today and the conflicting aims that often accompany it. Within SEE, TAP has proved to be simultaneously a boost to integration within the region and with the EU, a vital opportunity to diversify energy supplies and suppliers, a cause for conflict from competing supply routes and contentious politics in Turkey and Italy, and a possible captive to shifting geostrategic priorities with the rise of EastMed.

While these issues impact all countries in the region, the impact on Albania as a host to the pipeline itself promises to be both more significant and more challenging. TAP has proved to be an economic, political, and security windfall for Albania, but it poses new challenges through the environmental impact of increased hydrocarbon consumption, a higher dependency on energy imports, and greater rivalry from neighboring states.

Going forward, Albania should seek to actively mitigate these challenges and avoid falling victim to the shifting winds of geopolitics that have plagued energy transit states in the past. Possible steps might include broader stakeholder participation to address grievances from rural communities impacted by TAP, increased multilateral engagement with neighbors (particularly through the Energy Community), a sustained commitment to improving the investment climate, and more flexibility in adapting energy infrastructure for future changes, including the arrival of LNG, in order to remain a regional hub.

TAP has provided SEE and Albania with a unique and profitable opportunity based on the luck of geography, but it will require more than geography to ensure that these states take full advantage of TAP and avoid the pitfalls of global pipeline politics.

[1] “ESIA Albania – Non-Technical Summary,” Trans Adriatic Pipeline, 2012, https://www.tapag.com/assets/07.reference_documents/english/nts/albania/esia_nts_albania_in_english.pdf.

[2] “Commission Delegated Regulation (EU) 2018/540,” EUR-Lex, 23 November 2017, https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=uriserv:OJ.L_.2018.090.01.0038.01.ENG&toc=OJ:L:2018:090:TOC.

[3] Gas16 / Ionian Adriatic Pipeline (Fier, AL – Split, HR), Energy Community, https://www.energy-community.org/regionalinitiatives/infrastructure/PLIMA/Gas16.html.

[4] “Gas_13 / Albania – Kosovo* Gas Pipeline (ALKOGAP), Energy Community, https://www.energy-community.org/regionalinitiatives/infrastructure/PLIMA/Gas13.html.

[5] “Database,” Eurostat, https://ec.europa.eu/eurostat.

[6] Ibid.

[7] “Documents on creation of additional pipelines to join the Southern Gas Corridor were signed,” SOCAR, 16 February 2018, http://www.socar.az/socar/en/news-and-media/news-archives/news-archives/2018/02.

[8] Alissa de Carbonnel and Oleg Vukmanovic,“EU gets wake-up call as Gazprom eyes rival TAP pipeline,” Reuters, 14 February 2017, https://www.reuters.com/article/us-gazprom-eu-tap/eu-gets-wake-up-call-as-gazprom-eyes-rival-tap-pipeline-idUSKBN15T1LC.

[9] Massimiliano Di Giorgio, “Exclusive: Italy’s new government to review TAP gas pipeline,” Reuters, 6 June 2018, https://www.reuters.com/article/us-tap-italy-exclusive/exclusive-italys-new-government-to-review-tap-gas-pipeline-idUSKCN1J21SI.

[10] “EastMed pipeline plans regain momentum,” The Economist Intelligence Unit, 14 December 2017, http://www.eiu.com/industry/article/226231406/eastmed-pipeline-plans-regain-momentum/2017-12-14.

[11] Claudia Patricolo, “Albania’s Economy Not Benefitting From Largest Oil Reserves,” Emerging Europe, 28 November 2017, https://emerging-europe.com/in-brief/albanias-economy-not-benefiting-from-largest-oil-reserves-in-region/.

[12] “The Economic Impact of the Trans-Adriatic Pipeline on Albania: A report for TAP AG,” Oxford Economics, https://www.oxfordeconomics.com/Media/Default/economic-impact/economic-impact-home/Economic-Impact-trans-Adriatic-Pipeline.pdf.

[13] Ibid.

[14] Ibid.

[15] Ibid.

[16] “Land lost but not forgotten: Impacts of the Trans-Adriatic Pipeline on the land and livelihood o farmers in Albania,” CEE Bankwatch Network, November 2017, https://bankwatch.org/wp-content/uploads/2017/11/Land-lost-TAP.pdf.